Deoffshorization Law in Russia and possible solutions for the CFCs in Cyprus

The Federal Law No 376-FZ dated 24 November 2014 “Concerning the Introduction of Amendments to Parts One and Two of the Tax Code of the Russian Federation (Regarding the Taxation of the Profit of Controlled Foreign Companies and the Income of Foreign Organizations)” (the Law) was signed by President Putin on 24 November 2014 and entered into force on 1 January 2015. The Law introduces significant changes to the rules governing the reporting and taxation of participation interests by Russian tax residents in controlled foreign companies (CFCs) resulting in the profit of a CFC being imputed as taxable profit of a Russian tax resident controlling such a CFC at the usual Russian tax rate being 20 per cent for legal persons and 13 per cent for natural persons.

An overview of the key solutions that may circumvent the effect of the Law is provided below. We should note, however, several points that we consider are of an importance:

a. At this stage there is no universal solution and the advice we give hereto is always subject to review and confirmation as to its workability in Russian Federation by the Russian legal counsel re Tax position and treatment by tax authorities in Russia;

b. The Law has been prepared by hundreds of specialists whose sole aim was to cut off all old legal algorithms, which helped to optimize taxation;

c. The Law is likely to be amended to ‘soften’ the effect;

d. Each individual case should be treated on its merits and an individual solution to be found for each separate case scenario and wishes and abilities both monetary and non-monetary of the client to be taken into account.

Below, we are setting out key solutions, as we see them, under following headings:

1. Public companies– CypCo reconverts into PLC;

2. CypCo has two classes of shares: Voting and Non-voting Shares;

3. Creating substance in Cyprus and possible Naturalization via investment root;

4. Foundationsand trusts (non- corporate structures);

5. Creating a structure, whereby RusCo is a subsidiary of CypCo.

6. Life Insurance.

1. Public companies– CypCo reconverts into PLC

1.1. Public companies are in the exemption list but they should be listed on one of the recognized stock exchanges. That includes all Russian stock exchanges and all other stock exchanges to be approved by the Ministry of Finance of Russian Federation.

1.2. Otherwise, simply incorporating a public company would not be a solution and one will need to list the CypCo and that can be an expensive task. Also the issue of publicity must be considered in this case.

1.3 No shareholder of a public company should have more than 10% share of the PLC.

2. CypCo has two classes of shares: Voting and Non-voting Shares

2.1. We create a scheme whereby CypCo has two classes of shares: one class will be the managing shares with no right to receive dividends, and the second class of shares will not have any right of voting but right to receive the dividends;

2.2. In this way there shall be a clear division between two classes of shares, whereby, non-voting shares shall have a right to dividends but in no case shall they have powers to vote or any other residual powers attached to them, so that no control, as defined in the Law, is exercised;

2.3. The Articles of Association of CypCo shall be amended accordingly;

2.4. PWC (Russia) has adopted the above scheme for certain clients for which we have assisted them.

3. Creating substance in Cyprus and possible Naturalization via investment root

3.1 For a CypCo

(a) Creating substance in Cyprus i.e., real offices, payroll, real decision making happing in Cyprus (both strategic and day to day), corporate nominee directors not simply executing documents but asking questions etc,.

(b) For the purposes of determining Cyprus tax residency, one needs to pay attention and consider and request the advice in the jurisdiction where protection is thought, as Cyprus tax authorities are not likely to challenge such in Cyprus.

|

(c) For this purposes, below, we set out couple of considerations re test for the Tax residency for the purposes of taxation in Russian Federation:

(i) The test is the Test of Factual Control – key criteria:

(a) Board of Directors (over half of all the meetings take place in Russia);

(b) Executive management is predominantly performed from Russia;

(c) Chief Officers perform duties predominantly from Russia;

AND

(ii) Additional criteria (for cases where effective place of management qualifies in several countries):

(a) Accounting management accounting and office administration;

(b) Preparing and issuing strategically important corporate documentation;

(c) Operations management of employees.

SO, to determine tax residency in favor of Cyprus:

(iii) NOT ALLOWED:

(a) Relative majority of the Board of Directors in Russia;

(b) ‘Not substantially smaller’ presence of the executive body in Russia;

(c) Authorised people taking decisions in relation to day to day matters in Russia;

(d) Accounting, paperwork/clerical and operative management of the staff in Russia;

(iv) ALLOWED:

(a) Preparation and taking decisions at the GM level;

(b) Preparation for the Board Meetings;

(c) Intra-Group functions.

(d) Some practical considerations for the existing corporate structures - risks:

· UBO controls the activity of the group (CypCo can be treated as a Russian tax resident);

· Nominee directors, board meetings take place in Russia, no substance (Reduced tax rates under DTT may be denied, reporting obligations in Russia and taxation of undistributed profits in Russia as a consequence);

· Executive management and key officers perform duties from Russia, as well as accounting and staff management of all companies of the group (CypCo can be treated as a Rus. tax resident);

· UBO has a PoA for bank accounts and instructions to the bank given by the UBO (triggers obligation to report on participation in a CypCo and CypCo may be treated as Russian tax resident).

3.2. For an Individual - tax resident for the purposes of local tax laws and Naturalization via investment root

(a) In relation to the physical person thetax resident for the purposes of Cyprus tax Laws is liable to income tax in accordance with the Income Tax Law ( Law No. 118(I) of 2002 , as amended) in respect of their worldwide income. An individual is resident in Cyprus, if he/she resides therein for a period or more which in aggregate exceed 183 days.

(b) Other words, if an individual or his family members or his/her trusted person is/are prepared and ready to move to Cyprus and spend at least in aggregate exceeding 183 days in Cyprus he or she would qualify as a tax resident for the purposes of local tax laws and shall be taxed on his/her worldwide income in Cyprus.

(c) We also consider naturalization via Investment root as a great option for the high net worth individuals, who would want to invest in the Island. Depending on the magnitude of the proposed investment, the applicant can be granted with Cyprus nationality in the shortest periods of time. Please note that condition in 3.2 (b) above must, nonetheless, be satisfied. In this regards, we can provide further information upon request.

3.3 New Tax Law in Cyprus for Non-Domicile Persons

Cyprus Republic will soon adopt a new tax law (the so called ‘Non-Dom Tax Law’) pursuant to which a foreign person who would not spend more than 183 days in Cyprus, may be taxed in Cyprus, with a lower tax rate based only on his income collected in Cyprus (i.e. same tax laws as applied in certain cantons in Switzerland and other countries.)

The above law will make more attractive the implementation of the above scenarios.

4. Foundationsand Trusts (non- corporate structures). Cyprus International Trust with no residual powers on the settler and beneficiaries.

Foundationsand Trusts (non- corporate structures)are still in the Exemptions to the Law, but there are conditions:

(i) A settler/founder has no right to acquire ownership over assets transferred to the structure after it has been established; AND

(ii) A settlers/founder’s right related to his ‘personal status in the structure (including rights to dispose of property, to determine beneficiaries and other rights) cannot be transferred to other persons after the structure has been established’ unless by way of inheritance or universal succession; AND

(iii) A settler/founder cannot receive directly or indirectly (received by related person in his interest profits (income) of the structure distributed amongst the participants or beneficiaries (including Receipt of income by related person in the interest of a founder) AND

(iv) All above in accordance with the governing law and the foundations documents AND

(v) Exemption applies ONLY UNTIL the structure has no possibility to distribute profits (income) among participant beneficiaries, trustees and any other persons. There must exist NOT EVEN A POSSIBILITY of distribution of profits AND

(vi) Beneficiaries shall not have any residual power on the management of a trust (at all). For example profits are reinvested by the Trustee so that no funds to pass over to beneficiaries.

(vii) Exemption only applies if controlling persons reported participation in structures and provided documents confirming all above conditions are met.

Some practical considerations for wealth planning structures – effect on existing structures:

· Settler/founder must report participation in the structure irrespective of the residence status of the beneficiary;

· Russian resident beneficiaries are subject to reporting obligations;

· Settler/founder and or beneficiaries and/or other Russian resident persons considered controlling persons are subject to taxation of undistributed profits (income) at applicable rates.

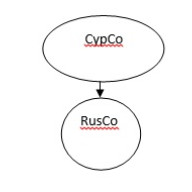

5. Creating a structure, whereby a RusCo is a 100% subsidiary of CypCo

In this way the CypCo becomes a 100% shareholder of the Russian company, hence, this particular structure does not give rise to reporting obligations under the Law but it should be kept in mind that nothing prevents Russian tax authorities from approaching Cyprus tax authorities for further information under the Exchange of Information provisions under the current DTT.

6. Put in Place Private Life Insurance

6.1. Firstly, we will use only the largest Swiss Insurance Companies based in the jurisdiction of Luxemburg for maximum Privacy and Security.

6.2. Private Placement Life Insurance has been used for many years in Europe as a compliant means of mitigation tax liabilities and adding security to company structures whilst maintaining privacy.

6.3. It has been used successfully to overcome similar legislation against controlled foreign companies in Europe and there has never been a tax assessment or court decision against Private Placement Life Insurance. All legal systems have contract law which recognizes life insurance policies, whilst not all recognize the concept of a trust or foundation;

6.4. Private Placement Life Insurance works in a similar way to a Trust but adds privacy, security, flexibility and substance;

6.5. The shares of CypCo holding company are transferred to the ownership of the Insurance Company, in return the client receives an insurance policy inside of which are his assets. Legally, all the client now owns is an insurance policy. The Insurance policy, however, belongs to him;

6.6. The structure with an existing trust can be used, nothing changes and the client will need to transfer the assets to insurance policy. The client can assign beneficiaries to the insurance policy to ensure continuity;

6.7. One of the problems of the trusts, foundations and investment funds is that the beneficial owner maintains control of the assets. With Private Placement Life Insurance an Asset Manager is employed by the insurance company (usually a corporate service provider) to manage the assets of the Insurance policy. In this way for legal purposes the client has no control of the assets. The beneficial owner is now the insurance company. The client is not a shareholder or a director of the insurance company and therefore not liable to reporting. This has the added benefit of giving the client creditor protection unparalleled in the corporate world. It is very difficult to legally attack an insurance structure.

Disadvantages/Risks

By adopting the above scheme the client/beneficiary might be held as ‘prisoner’ of the Insurance Company, because the client would not have any say on the management of the assets, neither any right to reverse the ownership or title of the asserts to him.

For further information on this topic please contact Mrs. Liza Bokova at SOTERIS PITTAS & CO LLC, by telephone (+357 25 028460) or by fax (+357 25 028461) or by e-mail (lbokova@pittaslegal.com).

The content of this article is intended to provide a general guide to the subject matter. Specialist advise should be sought about your specific circumstances.

![The Law amending the Companies Law CAP 113 N.4 [89(I) /2015] and collectively (the ‘Law’) came into force on 19 June 2015 and brought with it several changes to the current legal regime.](/images/thumbnails/mod_minifrontpagepro/c0e06a31051e0775970f657db2c09981_default.jpg)